Gen Z Credit Building 101: Why Credit Unions Are the Smart Choice

This article explains why credit unions are the ideal financial partner for Gen Z members looking to build credit from scratch. It covers the unique financial challenges facing Generation Z, including student loan debt, rising costs of living, and gig economy instability. It outlines why building credit early is critical to long-term financial health, specifically how credit history length impacts FICO scores. It details three credit union tools, including credit-builder loans, secured credit cards, and personalized financial guidance, that help young or thin-credit members establish a positive credit profile. The article positions Allied Solutions as a resource for credit unions seeking to attract and serve Gen Z through student lending programs and mortgage solutions.

For members of Gen Z, the world of personal finance can feel like a maze with no clear entry point. This generation is stepping into adulthood facing rising costs of living, student loan pressures, and a housing market that feels increasingly out of reach. This sentiment was reinforced by three of our summer 2025 interns in The Allied Angle podcast episode, "Gen Z Unfiltered."

One of the most foundational steps Gen Z can take toward addressing these challenges and contributing to long-term financial stability, building a strong credit history, often gets overlooked or misunderstood. The challenge is that building credit requires having credit in the first place, a frustrating catch-22 that leaves many young adults unsure of where to start.

That's where credit unions come in. Unlike traditional banks, credit unions are member-owned, not-for-profit financial institutions built around community, with missions that focus on people over profit. This makes them uniquely positioned to serve younger members who may have little to no credit history, limited income, or a distrust of conventional banking institutions.

Financial Challenges Facing Gen Z

Between cost of living, student loan payments, and a fluctuating housing market, Gen Z is stepping into one of the most precarious financial situations in a generation. The cost of nearly everything has surged, while entry-level wages have struggled to keep pace.

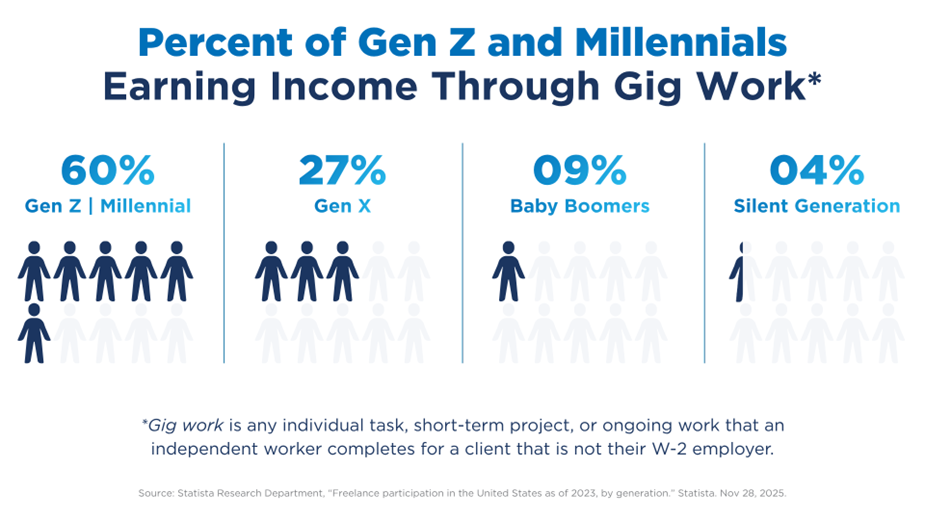

Beyond the big-picture economic pressures, Gen Z also faces a more fragmented financial landscape than any generation before them. Many are entering a workforce dominated by gig economy opportunities that offer flexibility but provide little in the way of employer-sponsored benefits, retirement plans, or long-term financial stability.

Building Credit Early Is Key

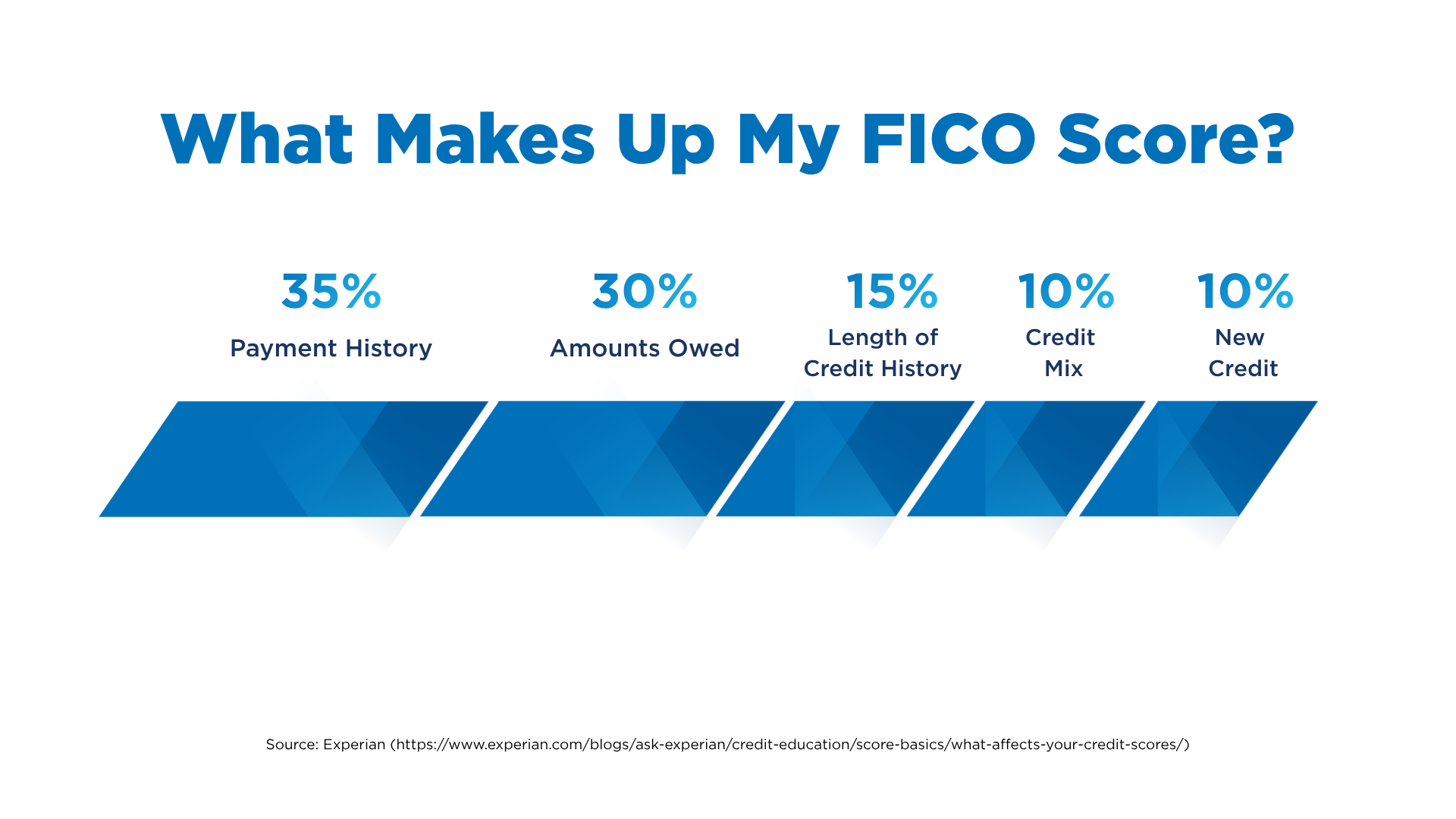

For Gen Z stepping into independence, a thin or nonexistent credit file can create friction in situations that have nothing to do with taking out a loan. Credit scores reward longevity. Since the length of your credit history accounts for roughly 15% of your FICO score, the earlier you open and responsibly manage an account, the more that history works in your favor over time.

A 22-year-old who opens a secured card today will have a decade of credit history by their early 30s, right when they're likely to be applying for mortgages, auto loans, or business financing. Waiting until you "need" credit is one of the costliest delays a young person can make.

See how student lending programs through Allied Solutions can attract and develop long-lasting relationships with Gen Z.

Credit Unions and Building Better Credit

Unlike traditional banks that are accountable to shareholders, credit unions are member-owned cooperatives whose primary goal is the financial well-being of their members. This fundamental difference in structure means credit unions are more likely to work with young adults who have little to no credit history.

One of the most powerful and underutilized tools credit unions offer is the credit-builder loan, a product specifically designed for people with little or no credit history. Unlike a traditional loan where you receive money upfront, a credit-builder loan holds the borrowed amount in a secured account while you make fixed monthly payments. Once the loan is paid off, you receive the funds and walk away with a track record of on-time payments reported to the credit bureaus.

Tools to Employ Now

- Credit-Builder Loans: Members make fixed monthly payments that are reported to the credit bureaus, building a positive payment history over time. Once the loan is paid off, they receive the funds, making it a smart way to build credit and savings simultaneously.

- Secured Credit Cards: Credit unions typically offer secured cards with lower fees and better terms than traditional banks. A small refundable deposit sets the credit limit, making it accessible for young adults just starting out. Used responsibly, a secured card is one of the fastest and most straightforward ways to establish a credit profile from scratch.

- Personalized Financial Guidance: Unlike big banks where interactions are increasingly automated, credit unions offer one-on-one financial counseling and education resources tailored to younger members.

Take advantage of Allied Solutions' mortgage servicers to provide healthy mortgage solutions to Gen Z and younger generations.

Credit unions provide the flexible approval criteria and specialized products necessary to help young or thin-credit members bridge the gap toward a secure financial future.