The Costliest Year of Fraud: Don't Get Spooked

Auto lenders face record fraud losses. This article explains where fraud enters the lending lifecycle, how vendor and infrastructure gaps increase exposure, and the practical controls that reduce losses: scaled AI decisioning, underwriting with fraud training, and enterprise cyber hygiene (MFA, encryption, EDR, patching, phishing simulations).

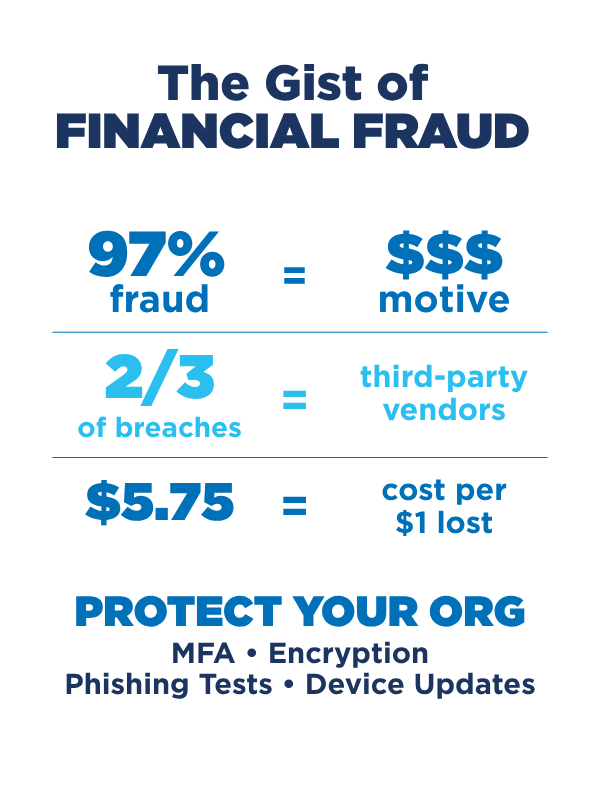

This year is shaping up to be the costliest year of fraud on record, with auto lenders alone bracing for $9.2 billion in losses.1

It isn’t only groceries and utilities feeling the sting of inflation, the cost of fraud remediation has inflated 44% in just four years.2

Where Is the Fraud Creeping In?

Fraud doesn’t have a single source, it creeps in through cracks across the lending ecosystem. Some of the biggest culprits include:

- Phantom paychecks: Misrepresented employment and inflated income on loan applications.

- Title trickery: Washing both paper and digital titles to hide damage.

- Psychologically spooky phishing: Complex, manipulative schemes that exploit human error and empathy.

Why It’s Frightening

Whether it’s skewing credit profiles, scrubbing damage history, or luring victims into giving away sensitive data, today’s fraudsters are more cunning than ever. These scares demand sharper vigilance and stronger protections before small leaks become monstrous losses.

Stronger Protections, Safer Lending

Most fraud is fueled by technology, but tech alone isn’t to blame. The real jump scare happens when infrastructure is fragmented and weak. Every weak link is a doorway for costly fraud.

Third-party technology is one of the most haunting risks, with a significant share of financial-institution breaches involving vendors.3 Lenders aren’t defenseless, though. You deserve the highest level of transparency from the partners who handle sensitive member and employee data.

That’s why Allied’s Trust Center exists, to give you confidence that your security is our top priority. Compliance, privacy, and reliability are at the heart of our products and services. At Allied, we believe stronger internal protocols plus more transparent vendor relationships are the silver bullet to shrinking fraud losses.

Best Practices to Keep the Fraud Scaries Away

Fraud may shift like shadows, but there’s no need to be spooked. These practices will shine a light on looming threats:

- Scale AI in credit decisioning. AI is a powerful tool for fraud management and response. Lenders eager to adopt should start small and scale upwards. For example, machine learning automation in credit decisioning can detect fraudulent information hidden in loan applications, flag anomalies faster than humans, and remove roadblocks for legitimate members. Leveraging AI decisions for this process removes roadblocks for legitimate member applications and can spot anomalies and fraud faster than humans. Implementing AI one area at a time can deliver lasting returns.

- Get insurance you can bank on. More stringent underwriting can reduce losses and should work hand in hand with proactive fraud detection. Enrich underwriting with fraud-prevention training so employees spot risk early and you stay confident while covered.

- Implement enterprise-wide cyber hygiene. Good cyber health is a shared responsibility. If you’re not already prioritizing cyber hygiene, now is the time to:

- Verify each access attempt, especially for new accounts.

- Encourage employees and members to freeze credit when appropriate.

- Activate multi-factor authentication for online banking.

- Encrypt data at rest and in transit, keep devices updated, and run regular phishing simulations and endpoint detection.

Cyber threats are getting trickier to predict, and it’s no treat to face them alone. With the right integrated solutions, proactive partnerships, and a culture of vigilance, you can protect your FI and safeguard the members you serve every day.

Keep the monsters of uncertainty away — subscribe for more fraud and security insights delivered straight to your inbox.